Instant and cross border payments are high on the list of priorities for businesses and authorities worldwide, yet interoperability and integration between different clearing systems has been a challenge hindering meaningful progression. That’s why ISO 20022

will be a

game changer once it becomes an official messaging standard. Yet for novices, this is a complex concept. This article is a beginner’s guide to ISO 20022 and why standardisation of financial messaging standards is so crucial.

What is ISO 20022?

ISO 20022 is an international messaging standard that offers transparency, speed and higher interoperability to the global payments sector. In simple terms, it’s an international standards framework that enables a common language for relaying electronic

messages between financial institutions. ISO 20022 will

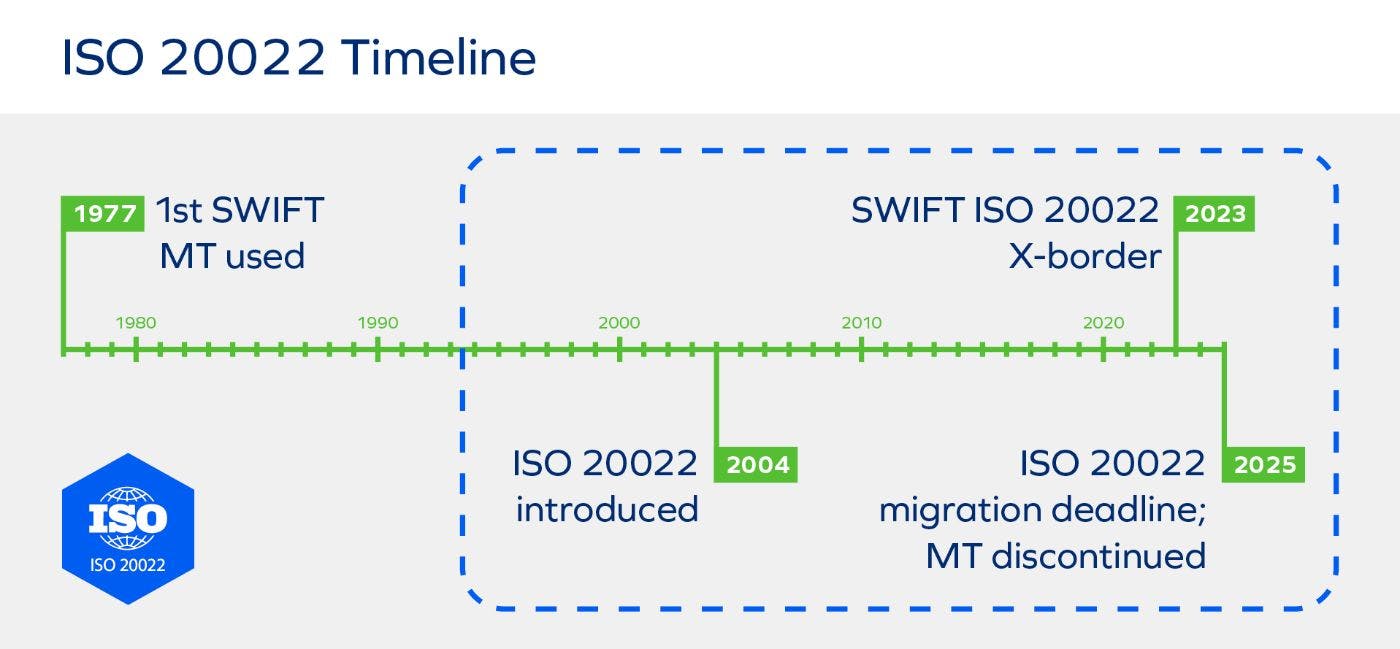

replace ISO 15022, which is the current messaging standard and has been developed in 1992.

(Source)

(Source)

When will ISO 20022 be implemented?

Migration to ISO 20022 started in Spring 2023 and is scheduled to be completed in November 2025. Yet while migration is underway, scepticism in the industry is high whether the deadlines can be achieved. The

European Payments Council (EPC) postponing its SEPA payment scheme migration has been but the latest example in dozens of ISO 20022

migration delays.

A recent

Celent survey of 211 global banks and corporates found that 1 in 4 banks believe the industry will not be ready by the migration deadline, with confidence running lowest in North America, where almost 1 in 2 is sceptic (72% and 56%). The upcoming year will

prove crucial for financial institutions to invest in technology and transformation to ensure their systems are ISO 20022-capable.

What makes ISO 20022 so useful?

The implementation of the ISO 20022 standard for global payments is a game changer in the industry. The comprehensive messaging standard will provide higher quality data which will enable enhance interoperability and higher quality payments in the global

financial industry. Some of the benefits ISO 20022 offers are:

- Streamlined processing time: Due to its global standardisation, ISO 20022 follows specific rules which enable bank systems to improve and accelerate payment validations. This will improve cross-border payment processing time.

- Richer data: As a messaging standing, ISO 20022 offers enriched data that allows banks to not just deliver faster services, but also to develop new products tailored to consumer behaviour. This can increase the speed of product innovation

in the entire sector.

- Higher accuracy: ISO 20022 doesn’t just hold structured data on payments, but on intermediaries as well. This allows banks to understand the full lifecycle of a payment and can lead to stronger forecasting capabilities and enhance accuracy,

i.e., in fraud investigations.

- Lower maintenance costs: As ISO 20022 is a unified standard across both the globe and the payments supply chain, it will allow businesses and authorities to improve both maintenance and Straight Through Processing (STP) rates.

- Enhanced regulatory compliance: Global identical protocols and formats, combined with access to richer data, will afford institutions a better ability of regulatory reporting, streamlined security procedures and validations.

- Reduced fraud: Similar to compliance, the enriched data that’s available through ISO 20022 will enable institutions to identify potential APP fraud cases more easily, reduce false positives and allows for more effective claims investigations

and management.